Last Tuesday I attended the Economist’s Bellwether Europe conference in London. Several speakers raised ideas that made me want to follow up Philippe’s latest piece “Has China Peaked?”.

At the conference, many speakers and panelist (from regulators like the FSA’s Martin Wheatley, to economists like Roubini’s Arnab Das, to portfolio managers like Blackrock’s Richard Kushel) linked the future stability of the Eurozone and the prosperity of America to the continued growth of China. Niall Ferguson was even more explicit, saying at one point that “The governor of the PBOC has far more control over the future of the US and European economies than either Ben Bernanke or Jean-Claude Trichet”. I tend to agree that US and EU economic stability is tied to Chinese growth, but am worried by that fact, and skeptical about Chinese “control” of their economy either through their Central Bank or through “administrative measures”.

The People's Bank

The image evoked by statements such as Ferguson’s (even though I am sure he is too smart to have intended it) is of a carefully calculating Zhou Xiachuan sitting behind a desk in Beijing pressing buttons and pulling levers – a man in commanding a linear, essentially Newtonian system. The same tends to happen when people talk about the powers and actions of the Fed and the ECB. Even so-called “centrally planned” economies don’t work like that. Economies are not not machines, and they are not linear in the sense that once the behavior of its component pieces are understood individually, one simply needs to add them up to predict – and control via a Central Bank or other bureaucracy – the behavior of the whole.

A point which is not original but which bears repeating because it is so often forgotten is that Economics is not Physics, it’s a “Social Science” (a false metaphor if there ever was one). As one scholar says “God gave Physics the easy problems” and the behavior of economies is non-linear rather than additive.

This idea is not new. It is what underpinned Hayek’s idea of catallaxy. It also stood behind his 1974 Nobel Prize lecture “The Pretense of Knowledge”. As Hayek said there, it is a mistake to grant economics “the dignity and prestige of the physical sciences”. (As I explored in Constructing Cassandra intelligence analysts are prone to make the same error, and slip towards scientism: “An exaggerated trust in the efficacy of the methods of natural science applied to all areas of investigation, as in philosophy, the social sciences, and the humanities.”)

In a key paragraph, Hayek said:

“Unlike the position that exists in the physical sciences, in economics and other disciplines that deal with essentially complex phenomena, the aspects of the events to be accounted for about which we can get quantitative data are necessarily limited and may not include the important ones. While in the physical sciences it is generally assumed, probably with good reason, that any important factor which determines the observed events will itself be directly observable and measurable, in the study of such complex phenomena as the market, which depend on the actions of many individuals, all the circumstances which will determine the outcome of a process, for reasons which I shall explain later, will hardly ever be fully known or measurable.”

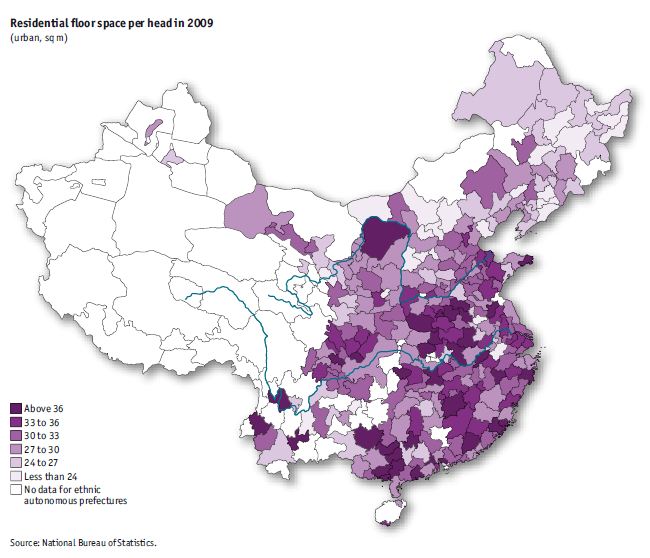

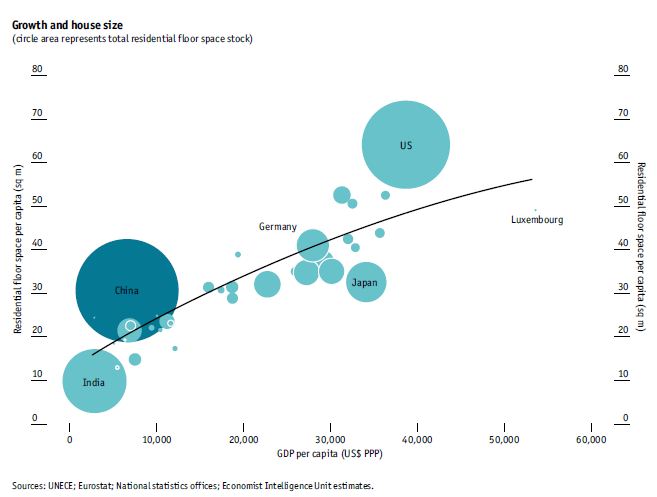

Which brings me back to China and the conference. I was especially struck by the charts displayed by the EIU from their new Whitepaper “Building Rome in a day: The sustainability of China’s housing boom”. Here are two:

Looking at these, one might be able to think of lots of explanations of why This Time is Different, and why despite its relative poverty (even measured by PPP), China has built so much residential floor space. If you can’t think of any, the EIU’s whitepaper helpfully points out: “a number of noteworthy characteristics in Chinese society that may account for the country’s housing exuberance,” and offers a menu of pre-rationalized explanatory options.

Is there a bubble in Chinese housing that could ripple through China’s – and the world’s – economy? I can’t say for certain. But like Hayek, I believe that there are “aspects of the events to be accounted for about which we can get quantitative data are necessarily limited and may not include the important ones.” This is especially so in a place like China, which has an economy at least partly predicated on central planning, with no independent political or press checks and balances, rife with perverse incentives and selective enforcement of laws, and moderately high corruption (despite regular executions to prevent it). And then there are anomalies that would trouble most experienced investors, like the fact that Beijing land prices have risen over 800% in the last seven years.

By the way: if you’re wondering whether Philippe’s “Uses of history for decision makers” is merely an academic exercise, I suggest the Jamestown Foundation’s series of pieces on how the Chinese leadership views the collapse of the Soviet Union. The Chinese leadership not only drew their own lessons from History, but they made sure that the Chinese people drew the “right” lessons by producing an eight-part television series called “Preparing for Danger in Times of Safety—Historic Lessons Learned from the Demise of Soviet Communism.”

I suspect the Chinese leadership knows that the potential for a non-linear disruption in China is not trivial. Maybe if Newtonian metaphors to describe economies are inevitable, the best one for China’s economy is a bus that dares not drop below a certain speed.

If you are interested in this topic, take a look at Philippe’s post: Has China peaked? An exercise in forecasting using Neustadt and May’s History framework.

PS If you find our perspective interesting, why not subscribe to our blog?

See also “Forget Greece: the euro is all about China” http://video.ft.com/v/969434002001/Forget-Greece-the-euro-is-all-about-China

Pingback: Business and Intelligence Techniques: the Role of Competing Hypotheses « Silberzahn & Jones

For information on the “squishiness” of Chinese inflation figures, see: http://www.businessweek.com/magazine/content/10_36/b4193007945730.htm

A nice update on the Zugzwang faced by the CCP is “Beijing Battles Brewing Crisis in Financial Sector” By Willy Lam in the latest China Brief from the Jamestown Foundation. See http://www.jamestown.org/uploads/media/cb_11_53.pdf (Zugzwang is a situation in chess in which any move you make weakens your position, but cannot be skipped).

These issues are further updated here: http://the-diplomat.com/2011/11/03/swimming-naked-in-china/?all=true

Here’s a nice summary from The Diplomat of China’s 2012 Challenges: http://the-diplomat.com/china-power/2012/01/08/chinas-2012-challenges/

I see from your bio you are in with the FT crowd, well maybe you can help them. Here is what you wrote and my analysis of where you are mixed up:

“Last Tuesday I attended the Economist’s Bellwether Europe conference in London… Many speakers linked the future stability and prosperity of the Eurozone and United States to the continued growth of China sustaining world growth. Niall Ferguson was even more explicit, saying at one point that “Economists in China have far more control over the future of the US and European economies than either Ben Bernanke or Jean-Claude Trichet”… The image evoked by statements such as Ferguson’s is of a carefully calculating Zhou Xiachuan sitting behind a desk in Beijing pressing buttons and pulling levers – an engineer in charge of a machine…. ”

“Yet I largely reject this imagery, economies are not not machines, they are chaotic system that need a good deal of intuition to run properly and are, in my opinion, frankly best left alone as much as possible. As one scholar famously said “God gave Physics the easy problems” and the behavior of economies is non-linear rather than additive…. ”

What you are saying here is that economics is bigger than engineering, it’s got psychology in as well. But in order to believe in democracy, you have to believe that what is even harder than maths is somehow the easiest thing in the world, something that people without either science skills or psychology can somehow make up as they go along. The journalists and politicians are experts in winning the hearts of crowds with simple emotional arguments, yet they claim to have this supreme skill of knowing how to instinctively answer everything. If journalists really knew all things then the best journalists would be the best philosophers and statesmen in the world, but the truth is they all disagree with each other and have no more professional consensus that a school yard of screaming kids.

Why is the “West” failing? Look at the comment by “MM in China” below. He says “I want the West to retain hegemony. If China ruled the world there would be no free press, it would be run by boring never wavering government experts instead of the crazy kids at the Economist and FT. I wouldn’t be able to watch porn on my computer or eat McDonalds because the scientists would have outlawed these things. I don’t want to live in the Platonic Republic of China, I want to live in a nice rich liberal democracy”. How do we answer him? First, you can’t have you cake and eat it. If you want to read bohemian newspapers and vote for bohemian politicians you are going to starve not thrive. Second, the place for democracy is in morality not economics. Give the people referendums on moral issues, let them decide the death penalty, junk food, gay marriage, porn and other moral issues themselves. Keep policy making in line with prevailing morality and make sure you retain popular support, but don’t let kids call the shots on economic issues. The great irony of the Philip Stephens type is that what he really promotes is the exact opposite: liberal dogma enforced by elite institutions to prevent the people beating up on sinners, and the total chaos of popular decision making in technical matters.